Weblog with daily updates of the news on a frugal, fair and beautiful China, from the perspective of internet entrepreneur, new media advisor and president of the China Speakers Bureau Fons Tuinstra

China protested against the US and Israeli attacks on Iran, but economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know® does not think this major upheaval will derail the planned meeting between US President Donald Trump and Chinese President Xi Jinping, he says at CNBC.

While there has been a shift in language on domestic consumption at the recent China’s annual Central Economic Work Conference, leading economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know®, does not see a change in policies for China’s economy in 2026 toward supporting the sluggish domestic consumption, he says at a debate at the Asia Society.

Leading China economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know®, looks at what is known about the upcoming 15th 5-year plan, bound to be approved by the National People’s Congress in March 2026. Most of the known information suggests no major changes, with an ongoing focus on manufacturing rather than consumption, as in the past, he tells Keith Yap in the Front Row Podcast.

Technically, the trade talks between China and the US, and even meetings between Xi and Trump, are on the agenda, but the US has quietly curtailed US exports to China in September, says business analyst Arthur Kroeberin the South China Morning Post. The ramifications of the US rule change became vividly apparent on September 30, when the Dutch government seized control of the chip firm Nexperia.

South China Morning Post:

Until recently, US exporters had to obtain a government licence to do business with any of the entities included on the lists. But in late September, the bureau broadened its rules: exporters now face restrictions not only when dealing with entities on the lists, but also with any company at least 50 per cent owned by entities on the lists.

US officials “depict this as a technical move” that closes an obvious loophole, but in reality “its impact is far from technical”, said Arthur Kroeber, partner and head of research at research firm Gavekal, in a research note published last week.

In practice, the new rules effectively expand the number of sanctioned companies, “probably by thousands or tens of thousands”, Kroeber said. Many of the companies affected by the rule change are Chinese.

What’s more, the new rules create an onerous compliance burden for businesses, as the responsibility for figuring out whether a given company is majority-owned by entities on the blacklists lies with US exporters. That means businesses must now conduct forensic due diligence on the ownership structure of many customers, Kroeber said.

The ramifications of the US rule change became vividly apparent on September 30, when the Dutch government seized control of the chip firm Nexperia.

Nexperia is a local company that in 2019 became majority owned by Wingtech, a Chinese chip firm that was put on the US entity list in 2021.

As Nexperia would be vulnerable to US sanctions under the new rules, the Dutch government’s move to take over the company and oust its Chinese CEO was necessary to preserve the firm’s unfettered access to the US market, Kroeber said.

Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know, discusses the state of China’s current economy at the Center for Strategic and International Studies on September 9. “So there are a lot of problems. It’s not vibrant from a consumer standpoint. But from a productive standpoint, there’s a lot that’s going right,” he says, according to Social News XYZ.

Social News XYZ:

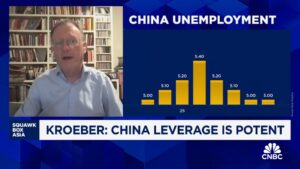

Key indicators reflected China’s factory output and retail sales going through their weakest growth since August last year. Retail sales have slumped, with demand at home weakening, and unemployment continued to tick up, said reports.

Industrial production rose just 5.2 per cent year‑on‑year in August, down from 5.7 per cent in July, and retail sales expanded only 3.4 per cent last month. It slipped from July’s 3.7 per cent, missing a forecast gain of 3.9 per cent.

Meanwhile, unemployment rate edged up to 5.3 per cent in August, while fixed‑asset investment grew a meagre 0.5 per cent in the first eight months – the weakest pace for that period since 2020 – and property investment collapsed nearly 12.9 per cent year‑on‑year through August.

Earlier this month, Arthur Kroeber, founder of Gavekal Dragonomics, a China-focused economic research firm, had pointed out: “You have a significant problem of persistent deflation, excess capacity in industry, declining profits, a weak job market, and a property market that’s in very poor shape.”

However, he soon added: “So there are a lot of problems. It’s not vibrant from a consumer standpoint. But from a productive standpoint, there’s a lot that’s going right.”

He was speaking at an event, hosted by the Washington-based Center for Strategic and International Studies on September 9.

Leading economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know®, explains at CNBC why China can walk away from a trade agreement with the US if they do not like it, although its economy is not very bright at this stage. He does not expect to see any great push to improve consumption or the economy at large, as the leadership is happy with the current modest growth.

Many observers wrongly see the current trade war between China and the US as a Cold War 2.0, says political analyst Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know® in an interview with Dwarkesh Patel. If American politicians started this war without seeing the difference from a cold war, it might be tough to bring it to an end, he adds.

Both China and the USA claim to want to negotiate a trade deal, but, according to economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know®, since there is no common agenda, only common mistrust, it appears very unlikely that these talks will progress. He says this in an interview at Dwarkesh Clips.

The Trump administration is pretty clueless on China, and that is only one of many issues when both countries are going to deal with each other, says leading economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know, in an interview with the Australian broadcaster ABC. Both can inflict huge damage on each other, but neither is in a position to win a full-blown trade war, he adds.

Today, Mr. Xi’s top priority economic strategy is to promote Chinese advanced, high-tech manufacturing, and he is pouring massive government investment into this task. In 2019 alone, China spent an estimated equivalent of 1.7% of its gross domestic product on industrial policy – four times that of the U.S., according to a CSIS study.

Such investments have led to successful Chinese innovation in key industries such as electric vehicles, and green energy transition products such as solar power equipment and lithium-ion batteries.

This dominance serves China’s goal to create a dense web of bilateral trade and investment ties that bolster its wealth and influence, while maintaining China as a fortress of industrial and technological self-sufficiency, says Arthur Kroeber, head of research at the financial services company Gavekal and author of “China’s Economy: What Everyone Needs To Know.”

“They want to have leverage over the rest of the world, which they think is best achieved through very deep economic ties,” he says. “If countries have a lot of eggs in the China basket, it’s less easy for them to rely on the U.S.”

China’s retaliation against Mr. Trump’s tariffs last Friday – imposing 34% in additional tariffs on all imports from the U.S., starting April 10 – shows that Beijing is calling Mr. Trump’s bluff, he says. After the first U.S.-China trade war launched by Mr. Trump in 2018, Beijing spent years fortifying itself against U.S. pressure and developing various retaliatory tools.

“The government believes China can sustain the pain longer than the U.S. consumer can … and the U.S. will cave first,” he says. As a result, in Beijing the plan is not to let Mr. Trump dictate the terms with his off-and-on tariffs.

“If you are China,” he asks, “do you have to play that game?”

Beijing may consider more drastic steps, such as devaluing its currency to make its exports cheaper, says Mr. Kroeber. Indeed, on Tuesday China’s central bank set its reference rate for the Chinese yuan at the lowest level since September 2023 – a move considered a warning signal to Washington.

Beijing’s propaganda apparatus is working overtime to signal resolve.

Much attention goes to industrial innovation to save China’s sluggish economy. But leading economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know®, is not too sure that path is helping the economy, he tells at NPR. “Growth is probably going to be pretty sluggish for a few more years yet. And they’re not going to get this magical nirvana that they hope for,” he adds

NPR:

WOODS: But the strategy may have its limitations, according to Arthur Kroeber. Arthur is one of these long-time China heads. He’s written a book. He started a China macroeconomics firm. He divides his time between New York and Beijing. He says that the government’s theory seems to be that heavy investments in tech will lead to productivity breakthroughs. Those productivity breakthroughs will then lead to higher wages and good jobs

ARTHUR KROEBER: I don’t think that that is very likely, because the problem with that is you look at all these high-tech industries that everyone is so excited about, EVs and batteries and whatnot, but they’re not very profitable.

RUWITCH: Arthur says there’s a capacity glut, a lot of stuff being produced, but not enough buyers to keep businesses standing on their own two feet. Companies in the solar sector are struggling. In batteries, profits are falling. Profitability in EVs is dropping. And a lot of this is due to competition with other companies in China.

KROEBER: Everyone is struggling, so they’re all barely making money. And so they don’t have a lot of ability to hire lots of people and give them big wages.

WOODS: Without those big wage increases, Arthur says, it’s hard to see how growth in high-tech industries will spill over to the rest of the economy.

RUWITCH: He says China’s industrial policy has been successful at a certain level.

KROEBER: They’ve got a lot of very competitive manufacturing industries. But the– but growth is probably going to be pretty sluggish for a few more years yet. And they’re not going to get this magical nirvana that they hope for.

While in the past youth looked for jobs in the private sector or at foreign companies, they now look for government jobs as they offer more security, says Arthur Kroeber, leading economist and author of China’s Economy: What Everyone Needs to Know®. Most graduates feel the sluggish Chinese economy will continue for some time, he says on CNBC.

China has started to push capital into its sluggish economy, but economists have different opinions on what the government wants to achieve. According to Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know®, its financial measures are more about stabilizing its economy, not about a full-blown stimulus as it did in the past, he says at the ChinaFile.

Arthur Kroeber:

China’s economic support measures are better described as stabilization than stimulus. Unlike in previous full-bore stimulus programs, for instance in 2008 and 2015, the aim today is not to engineer a boom but simply to halt the deterioration in economic conditions evident in the past few months, and stabilize growth at around the target of 5 percent.

China’s long-term economic strategy has not changed. Xi Jinping’s intent, as outlined in the Third Plenum decision this past July, is to shift capital from real estate and infrastructure into technology-intensive manufacturing. The aspiration is that the productivity gains from high-tech industries will deliver the long-run growth that China needs, offsetting the impact of a declining population and other negative factors. Another key goal of this strategy is to ensure that China becomes self-sufficient in core technologies, enabling it to withstand the pressure of U.S. containment policies. The leadership is fully prepared to tolerate a period of relatively sluggish growth as the price of making this structural shift.

But the stabilization policies of the last month show the limits of this tolerance. They also reflect a judgment that the contraction of the property sector, now into its fourth year, has gone far enough, and that policy should shift from restrictive to modestly supportive. The final policy move, expected in early November—issuance of long-term central government debt to swap for provincial debt—is a long-overdue recognition that the financial position of heavily indebted provinces is unsustainable, and that direct fiscal support from Beijing is needed.

Over the next year or so, the economic package is likely to succeed in its limited aims: reversing the decline in housing sales, and providing local governments with relief from interest payments so they can pay back wages to their employees and overdue bills to the companies that supply them with goods and services. This should be enough to stabilize GDP growth at somewhere close to the 5 percent target. The benefits to the rest of the world, however, will be modest. Neither consumer spending nor commodity demand will enjoy a dramatic pickup. And Beijing’s steady commitment to its investment-first growth strategy means that other countries will still face the challenge of intense competition from low-priced Chinese imports.

Despite the hope of the international financial community, China is not heading for structural reforms, says leading economist Arthur Kroeber, author of China’s Economy: What Everyone Needs to Know®, to CNBC. Pushing up demand is not high on the agenda for China’s leadership, he says, and they do not want to push up debts levels to new heights.

China might have the upper hand in dealing with the US president’s efforts to curtail the country’s economy with sky-high tariffs, suggests

China might have the upper hand in dealing with the US president’s efforts to curtail the country’s economy with sky-high tariffs, suggests